|

The President is proposing that Congress pass two temporary expansions of critical Small Business Administration (SBA) lending programs. These are both legislative proposals designed to help small businesses through what continues to be a difficult period in credit markets.

1. Expand SBA's existing program to temporarily support refinancing for owner-occupied commercial real estate loans: Eligible small businesses will have commercial first mortgage loans or existing 504 first mortgage loans that are maturing in the next year. In order to qualify, businesses will have to be current on all loan payments for the previous year. Lenders that are refinancing mortgages for existing customers will make a loan http://www.Halocapitalgroup.com for up to 70 percent of the current property value; and SBA will help finance the remaining 20 percent. For new lenders taking on a refinancing project, SBA will take on a greater share of financing, up to 40 percent. SBA's proposal for a temporary, zero-subsidy CRE refinancing program would be funded through additional fees for refinancing projects, not through a Congressional appropriation. This proposal will help refinance up to $18.7 billion each year in commercial real estate that might otherwise be foreclosed and liquidated. 2. Temporarily increase the cap on SBA Express loans from $350,000 to $1 million: The President is proposing to temporarily increase the maximum SBA Express loan size to $1 million, which would expand the program's ability to help a broad range of small businesses. Unlike traditional 7(a) loans, lenders can use their own paperwork for SBA Express loans, which can be structured as revolving lines of credit. Currently, these Express loans are capped at $350,000 and carry a 50 percent guarantee. Fees would cover virtually all of the added costs of this proposal. These proposals complement the President's broader small business agenda - a key part of his overall jobs plan. The other elements of the small business agenda include: o Extending small business expensing and bonus depreciation for 2010. Eliminating https://en.wikipedia.org/wiki/Commercial_mortgage capital gains for small businesses in 2010.  o A Small Business Jobs and Wages Tax Credit that would cut taxes for more than 1 million small businesses by paying up to $5,000 for every net new job and covers payroll taxes on overall wage increases in excess of inflation. o A $30 billion Small Business Lending Fund to provide capital for community banks and an incentive to increase lending to small businesses. o Additional SBA lending proposals, including an extension of the Recovery Act programs that eliminate fees and raise guarantees on 7(a) loans and permanent increases in the maximum loan sizes for major SBA programs.  http://www.foxnews.com/politics/2010/02/05/obama-prposes-expansions-sba-lending-programs.html

0 Comments

Automatic emergency braking can help prevent car crashes or reduce their severity by...

The agreement announced today affects nearly all light-duty cars and trucks with a... This agreement will expedite automatic emergency braking standards three years faster... Every time a new safety technology becomes standard on modern cars it adds to the costs... " newsbulletin.nbFooter = "" //append widget header $("#newsbulletin > .midcontainer").append(""); $("#newsbulletin > .midcontainer").append(newsbulletin.nbContainer); $("#newsbulletin > .midcontainer").append(newsbulletin.nbFooter); newsbulletin.nbDiv = document.getElementById('nbItemContainer'); nbjsId = 0; newsbulletin.load = function() //alert(newsbulletin.baseloc+'/xmldata/newsbulletin?id=14640490&twOverride=&lpos='+newsbulletin.lpos+'§ion=&'+nbjsId) //to try and handle caching in webkit browsers dynamicJS.load('newsBulletin'+nbjsId, newsbulletin.baseloc+'/xmldata/newsbulletin?id=14640490&twOverride=&lpos='+newsbulletin.lpos2+'§ion=&'+nbjsId); //dynamicJS.load('newsBulletin','http://preview.abcnews.go.com/xmldata/newsbulletin?id=13564505'); //display items newsbulletin.displayItems = function(nbItemObj) //check if status update this.isStatusUpdate = (nbItemObj.label == 'Status Update')?true:false; //item type class this.itemTypeClass = (this.isStatusUpdate)?'orange':'blue'; //bg position this.itemBgPos = '100% 55%'; if(nbItemObj.bgPos != null) this.itemBgPos = nbItemObj.bgPos; //author image this.nbItemStyle = ''; this.nbH4Class = 'class=nbheader'; this.nbH4Style = ''; this.nbItemStyleAuthor = ''; if(nbItemObj.authorimage != null && nbItemObj.authorimage != '') this.nbH4Style = ' style=width:210px;'; this.nbItemStyle = 'background:url('+nbItemObj.authorimage+') no-repeat bottom right'//+ this.itemBgPos; this.nbItemStyleAuthor = ' nbItemContentsAuthor' //title this.title = ' '+nbItemObj.title+' '; if(nbItemObj.link != null && nbItemObj.link != '') this.title = '' //text this.text = ''; this.textCapped = ''; this.morelink = 'More' if(nbItemObj.text != null) this.text = nbItemObj.text; //if item is not expanded display capped text if applicable if(nbItemObj.isExpanded != true) if(nbItemObj.text.length > 63) this.textCapped = nbItemObj.text.substring(0, 63); this.text = this.textCapped + '...'; if(this.isStatusUpdate) this.text = this.textCapped + '... ' + this.morelink; //social this.social = ''; this.socialStyle = ''; this.authorBlock = ''; this.divider = ''; this.fb = ''; if(nbItemObj.authorfb != null && nbItemObj.authorfb != '') this.fb = '' this.twitter = ''; if(nbItemObj.authortwitter != null && nbItemObj.authortwitter != '') this.twitter = '' this.bio = ''; if(nbItemObj.authorbio != null && nbItemObj.authorbio != '') this.bio = ''+nbItemObj.author+'' this.authorBlock = ' '+this.bio+' ' if(nbItemObj.author != null && nbItemObj.author != '') this.twitter != '') this.socialCustomStyle = ''; this.social = this.fb + this.twitter; this.socialStyle = ' style="height:21px; padding: 2px 0px;' + this.socialCustomStyle + '"'; else this.social = ''; this.textStyle = ''; if(nbItemObj.authorimage != null && nbItemObj.authorimage != '') this.textStyle = ' style=width:208px;'; else this.categoryTag = ''; this.nbTextOverride = ''; this.rowTemp = ''+this.title+' '+nbItemObj.date+' '+this.authorBlock+' '+this.text+' '+this.social+' '; if (nbItemObj.notes) nbNotes = nbItemObj.notes; nbNoteStr = ''; nbNoteDivider = ''; $.each(nbNotes, function(idx) nbNote = nbNotes[idx]; this.noteAuthorBlock = ''; this.notefb = ''; if(nbNote.noteAuthor.facebook != null && nbNote.noteAuthor.facebook != '') this.notefb = '' this.notetwitter = ''; if(nbNote.noteAuthor.twitter != null && nbNote.noteAuthor.twitter != '') this.notetwitter = '' this.notebio = ''; if(nbNote.noteAuthor.bio != null && nbNote.noteAuthor.bio != '') this.notebio = ''+nbNote.noteAuthor.name+'' this.noteAuthorBlock = ' '+this.notebio+' ' this.notesocial = ''; this.noteSocialStyle = ''; if(nbNote.noteAuthor.name != null && nbNote.noteAuthor.name != '')else this.notesocial = ''; if (idx == nbNotes.length-1) nbNoteDivider = '';  this.nbNoteDiv = ' '+nbNote.noteHeadline+' '+this.noteAuthorBlock+' '+nbNote.noteOverview+' '+this.notesocial+' '; nbNoteStr += this.nbNoteDiv; ); this.rowTemp += nbNoteStr; return this.rowTemp; function showMoreText(id) //grab old item height var oldItemHeight = $('#nbItem_'+id).height(); //retrieve the content from the array $('#text_'+id).html(contentObject[id]) //store id a list of opened objects fullTextList.push(id.toString()); var newContainerHeight = $("#nbItemContainer").height() + ($('#nbItem_'+id).height()-oldItemHeight); $("#nbItemContainer").css('height', newContainerHeight); //reinitialize scroll window.api.reinitialise(); lastNBObjStr = ''; function isNewData(data) isNewTemp = false; currNBObjStr = ''; $.each(data.updates, function(ind) currNBObjStr = currNBObjStr + data.updates[ind].objId + data.updates[ind].date; ); //console.log('x'+currNBObjStr); //console.log('y'+lastNBObjStr); if(currNBObjStr != lastNBObjStr) isNewTemp = true; else //console.log('no refresh'); lastNBObjStr = currNBObjStr; return isNewTemp; isHeaderLinkLoaded = false; // flag to check if the header link is loaded isShareLinkLoaded = false; // flag to check if the share link is loaded isDoneLoading = false; // flag to check if the html is done loading in the jScrollPane function newsBulletin(data) if(data) isNewDataFlag = isNewData(data); if(isNewDataFlag) //clear contents first newsbulletin.nbDiv.innerHTML = ''; //console.log('refresh'); updates = data.updates; headerLink = data.widgetLink; shareLink = data.shareLink; if (headerLink != '' && headerLink != null && !isHeaderLinkLoaded) var twitterImg = " $("#newsbulletin > .midcontainer > .widget_head").append(""); $("#newsbulletin > .midcontainer > .widget_head > .twitterLink a > .twitterContent").append("" + twitterImg + ""); isHeaderLinkLoaded = true; //clear the author cutouts array newsbulletin.authorCutouts = []; // check to see if there is a height set for container, if so clear it // prevents cacheing var hasHeight = $('#nbItemContainer').attr('style'); if (typeof hasHeight != 'undefined') $('#nbItemContainer').removeAttr('style'); /image3.jpeg) $.each(updates, function(ind) var itemDetails = new Object(); it = updates[ind]; //populate the itemDetails object itemDetails.id = it.objId; itemDetails.title = it.title; itemDetails.objType = it.objType; itemDetails.link = it.link; itemDetails.date = it.date; itemDetails.label = it.label; itemDetails.author = it.author.name; itemDetails.authorbio = it.author.bio; itemDetails.authorfb = it.author.facebook; itemDetails.authortwitter = it.author.twitter; itemDetails.feed = it.feed; itemDetails.category = it.category; //set defaults if item is a status update if(itemDetails.label == 'Status Update') if(it.author.image == '') it.author.image = 'http://a.abcnews.com/assets/images/abc_news_logo_84x84.png' if(it.author.name == '') itemDetails.author = 'ABC News' itemDetails.authorfb = 'http://www.facebook.com/abcnews' itemDetails.authortwitter = 'http://twitter.com/abc' //only pass the author image if it's not displayed in any of Halo Capital Group the items yet if($.inArray(it.author.image, newsbulletin.authorCutouts) == -1) itemDetails.authorimage = it.author.image; //add to ignore list if(it.author.image != '' &&($.inArray(it.author.image, newsbulletin.authorCutouts) == -1)) newsbulletin.authorCutouts.push(it.author.image); if(it.text != '') itemDetails.text = it.text; else itemDetails.bgPos = 'bottom right'; if (it.notes) itemDetails.notes = it.notes; //build a name value pair list of id/text contentObject[itemDetails.id] = itemDetails.text itemDetails.isExpanded = ($.inArray(itemDetails.id, fullTextList) > -1) ? true : false; //build markup $("#nbItemContainer").append(newsbulletin.displayItems(itemDetails)); ); $("#nbItemContainer").append(''); //set the height of container div $("#nbItemContainer").css('height',$("#nbItemContainer").height()); if (shareLink != '' && shareLink != null && !isShareLinkLoaded) $("#newsbulletin > .midcontainer > .nbFooter").css("height":"35px", "border-top":"1px solid #d5d5d5", "border-bottom":"border-bottom:1px solid #eaeaea"); $("#newsbulletin > .midcontainer > .nbFooter").append(""); isShareLinkLoaded = true; if($.browser.msie) if ($.browser.version .midcontainer > .nbFooter").css("display":"none"); var timeoutId = setTimeout(function() $("#newsbulletin > .midcontainer > .nbFooter").css("display":"block"); clearTimeout(timeoutId); , 3000); dynamicJS.unload('newsBulletin'+nbjsId, newsbulletin.baseloc+'/xmldata/newsbulletin?id=14640490&'+nbjsId); isDoneLoading = true; if ($.browser.webkit) if(nbjsId .midcontainer > .nbFooter").css("display":"none"); var timeoutId = setTimeout(function() $("#newsbulletin > .midcontainer > .nbFooter").css("display":"block"); clearTimeout(timeoutId); , 3000); 7500) setInterval( function() window.api.getContentPane().html( newsbulletin.load() ); , 120000 ); setInterval(function() // we could call "pane.jScrollPane(settings)" again but it is // more convenient to call via the API as then the original // settings we passed in are automatically remembered. // Initialization of the container should be done after all the markup has been loaded // since there is no listener that could be passed into reinitialise() for callback if (isDoneLoading) window.api.reinitialise(); isDoneLoading = false; , 5000); ; addOnload(newsbulletin.load()); http://abcnews.go.com/business Connect Most stock quote data provided by BATS. Market indices are shown in real time, except for the DJIA, which is delayed by two minutes. All times are ET. Disclaimer. Morningstar: © 2016 Morningstar, Inc. All Rights Reserved. Factset: FactSet Research Systems Inc. 2016. All rights reserved. Chicago Mercantile Association: Certain market data is the property of Chicago Mercantile Exchange Inc. and its licensors. All rights reserved. Dow Jones: The Dow Jones branded indices are proprietary to and are calculated, distributed and marketed by DJI Opco, a subsidiary of S&P Dow Jones Indices LLC https://halocapitalgroup.com/small-business-loan-interest-rates-and-terms and have been licensed for use to S&P Opco, LLC and CNN. Standard & Poor's and S&P are registered trademarks of Standard & Poor's Financial Services LLC and Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC. All content of the http://www.realestateabc.com/loanguide/applying-commercial1.htm Dow Jones branded indices © S&P Dow Jones Indices LLC 2016 and/or its affiliates.  © 2016 Cable News Network. A Time Warner Company. All Rights Reserved. Terms under which this service is provided to you. Privacy Policy. . http://money.cnn.com/news/ NEW YORK (CNNMoney.com) -- Bank lending to small businesses has dried up in recent months. One reason credit has grown scarce: They're risky loans. A new analysis of Small Business Administration-backed loans found that the failure rate has hit the double digits, with 11.9% of the SBA's loans last year going into default.

The Coleman Report, which provides lenders with small business data and SBA news, calculated the failure rate by dividing the number of loans liquidated or charged-off last year by the total number of loans made through the SBA's flagship lending programs.  Last year's failure rate is a sharp increase over past years. In 2004, the SBA loan failure rate was 2.4%, but it has increased each year since, rising to 8.4% in 2007, according to Coleman's calculations. The 2008 failure rate of nearly 12% covers the fiscal year that ended on Sept. 30. In that year, the SBA's 7(a) and 504 programs approved 78,324 loans, totaling $18.2 billion. "The numbers are brutal, but it validates what we already know," said the report's editor and publisher, Robert Coleman. "In towns, we see established businesses going under every day, and [I've heard] bankers say their small business portfolios have become a disaster." Doing its own calculations based on defaults in December - which falls in the agency's 2009 fiscal year - the SBA came up with a annualized default rate of around 5%, based on the total dollars lent. Calculating defaults based on the number of loans made, the default rate for the 2008 calendar year was around 10%, according to the SBA.  "The real point is, of course, that both rates - number of loans and dollars - have been rising. That increase is a reflection of what's going on in the general economy," said SBA spokesperson Mike Stamler. "It could not be a surprise to anyone that loan defaults rise when the economy turns difficult, and the economy has been getting more and more difficult for some time now." The SBA's loan programs offer banks insurance on a percentage of qualifying small business loans: If the borrower defaults, the SBA pays the bank back for the portion of the loan it has guaranteed. This approach makes small business loans more enticing to risk-averse lenders. But the number of loans the SBA backed plunged in 2008, thanks to stricter bank lending standards and a frozen secondary market for the loans. "Lenders are criticized for not getting capital to Main Street, but the problem, as this report shows, is that it's hard to justify getting capital out there when there's a 12% failure rate," Coleman said. "That's why they tightened the credit box." Congress has picked up on the problem. The stimulus bill passed last week included a provision allowing the SBA to increase its guarantees to 90% of qualifying loans, up from a current maximum of 85%. But that won't solve the problem of loan failures - it will only transfer the losses from banks to the government. The SBA's loan charge-off rate - the actual cash paid by the agency to honor its guarantees divided by the total dollars disbursed - has increased from 0.4% in 2004 to 1.9% last year, according to The Coleman Report. "Credit got easier, and there was too much capital for too little demand. So more and more loans went out to those who were going to fail," Coleman said. "But now we have the opposite problem, and the clamp-down has made loans too scarce." "The magnitude of the credit crunch, a uniquely cruel feature of this particular recession, only makes things worse," said the SBA's Stamler. "This situation won't turn around until we can get capital flowing again to small businesses. That's what the TARP and the TALF and the recovery act are designed to do." In the meantime, while the government and lenders try to find that steady middle-ground for small business lending initiatives, Coleman suggests the SBA and lenders try to curb the fear they're bound to feel when they see the grim statistics. "We all want to be good stewards of tax payers' dollars," Coleman said. "Because 50% of the GDP is driven by small businesses, we need to focus on the flip argument: There's an 88% success rate. Just face that we will have losses right now, and that those losses have to be at the government level so that we can protect what we have." First Published: February 25, 2009: 10:48 AM ET To write a note to the editor about this article, click here. http://money.cnn.com/2009/02/25/smallbusiness/smallbiz_loan_defaults_soar.smb/ Is your business suffering and you are seeking instant monetary support for your business then you can either opt for the route that many other business organizations in the United Kingdom opt or sell off your inventory. The choice is yours. Business loan is what a large number of companies look forward to when seeking immediate cash. These loans can be availed as per your wish and requirement. You can start a business or expand the new one. Funds availed through this loan can be acquired by anyone who is a citizen of United Kingdom and wants to create a niche in the market. Many young business entrepreneurs have been applying for it to realize their business dreams.

With this kind of loan facility, you can buy raw material, equipments or office furniture to stay ahead in this highly competitive business world where various businesses of the same nature crop-up every other day. These loans are a sure-shot way to survive here and emerge as winners. In addition to this, you can hire more employees to offer quality customer service to all clients and promote your business like you always desired for. Whether it is cash that a borrower need desperately or you simply wish to spruce up your current business, these loans can do it for you without delay. More often than not, a young business entrepreneur approaches either money-lending firms or banks for a loan needed to start a business. However, in this day and age, you can apply for it from the comfort of your home. It is the online mode of application that has enabled a large number of people to fetch instant funds. Internet is just the right destination to search for such loans. Ever mounting competition amidst online money-lenders has proved beneficial for borrowers for they have a range of options to choose from. You can choose the one that fits your existing business needs and is available at reasonable interest rates. Even those having faltering credit background can finance their new business with this amazing loan facility. Obtaining this financial assistance is not at all an easy job if you are living with tags like insolvency, county court judgments, arrears, foreclosures, non payments or late payments, individual voluntary arrangements or defaults. However, with this loan facility even they can grab funds without giving a second thought.  Business loans tend to carry a high rate of interest. It is, therefore, suggested that you avail this loan after conducting a proper research. Make sure that you spend the acquired amount carefully so that you have sufficient funds at the later stage. Compare online quotes before making any decision. Funds to start a new business are just a few clicks away. http://www.articlecity.com/articles/business_and_finance/article_16051.shtml Bad gateway

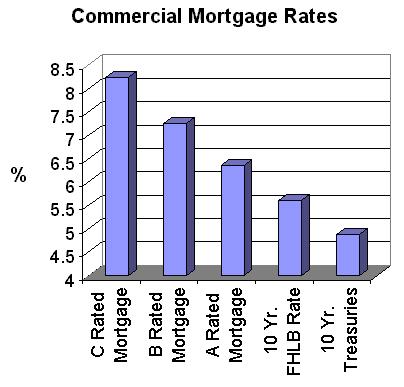

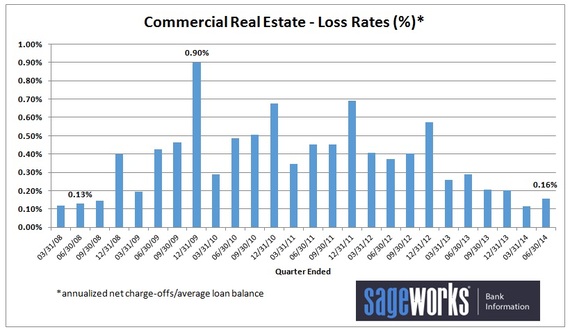

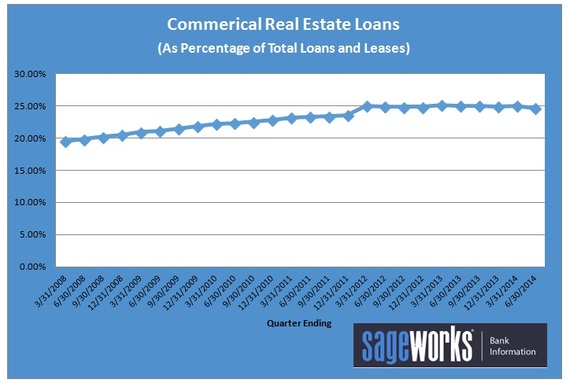

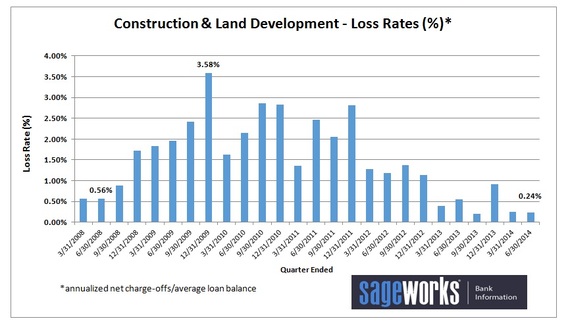

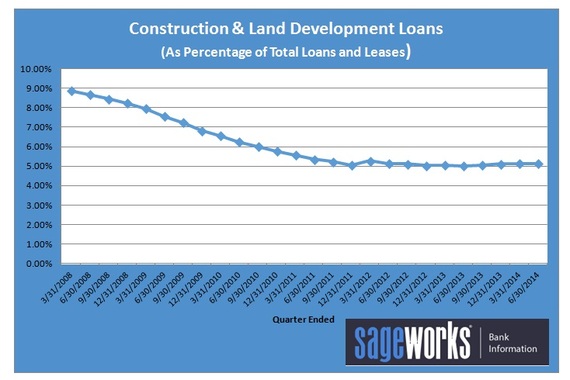

San Jose CloudFlare Working www.articlesnatch.com Host Error  What happened? The web server reported a bad gateway error. What can I do? Please try again in a few minutes. http://www.articlesnatch.com/blog/Small-Business-Loans--Loan-With-No-Collateral/872180  U.S. banks are seeing some of the lowest loss rates of the past six years on commercial real estate and construction loans, boosting their case for increased lending activity in the sector. Data from Sageworks, a financial information company, show that net charge-offs for commercial real estate loans (non-farm, non-residential) were 0.16 percent of average loan balances in the most recent quarter. This is down from 0.9 percent at the end of 2009 and 13 basis points below June 2013 quarter rates. Loss rates for construction and land development loans have fallen from 3.58 percent of average loan balances in December 2009 to 0.24 percent in the most recent quarter. Sageworks analyst Regan Camp said that in addition to falling loss rates, the improving economy and increased competition for attractive borrowers in the commercial and industrial lending space may also contribute to a sense of confidence in lending activity in this sector.  "The good news is that as more banks move back into real estate lending, it will present more options for borrowers," Camp said. Increased competition for borrowers might allow for more appealing terms or incentives, he noted. Indeed, the Federal Reserve's recent Senior Loan Officer Opinion Survey found banks on balance have been easing standards on most types of commercial real estate. And the FDIC's latest quarterly report showed banks' commercial real estate lending has increased to levels unseen since 2007. For several years, Camp said, banks moved away from commercial real estate lending because of losses tied to real estate loans before the Great Recession. Demand, too, had been weak as contractors and investors either collapsed or backed off dramatically in the wake of real estate market woes.   But the Mortgage Bankers Association noted recently that commercial bank portfolio loans for commercial and multifamily mortgage loans increased 19 percent in the second quarter from a year earlier. Meanwhile, the dollar volume of commercial/multifamily mortgage loans originated for Fannie Mae, Freddie Mac and commercial life insurance companies decreased in the same period. Other reports have noted increased lending for residential and commercial construction projects as more banks of all sizes have entered the space. Fitch Ratings expects commercial construction activity will continue to be fueled by easing lending standards and improving industry fundamentals. "Initially, the early movers jumped on the C&I lending wave, and there were probably a lot of opportunities there for banks," Camp said. "As more lenders move to that, all of sudden there's not as much opportunity, so banks may be saying, 'Let's back off and go back to the lending that we know, and the lending that we know and opportunities that have been there are in commercial real estate.'" Commercial real estate loans as a percentage of total loans and leases at U.S. banks have slowly increased since 2008. These loans now make up 24.68 percent of portfolios, compared to 19.55 percent as of March 2008, according to data from Sageworks Bank Information, a web-based data platform. Construction and land development loans were 5.14 percent of total loans and leases in the June-ended quarter, down from 8.88 percent in March 2008. Low demand for credit and fewer credit-worthy projects were the biggest challenges for banks in making commercial real estate loans, according to a survey released in April by the American Banking Association. But hard caps on commercial real estate lending imposed by regulators and other supervisory requirements were cited 22 percent of the time in the survey. Camp said that risk is an important factor for banks, which are under increased regulatory scrutiny and requirements to adequately stress test their commercial real estate portfolios. "Banks have been burned before and regulators want to know, did they learn their lesson?" he said. "Even though confidence has come back significantly, I don't think anyone's one hundred percent certain it won't happen again." A recent report by the Real Estate Research Corporation (RERC) cautioned that increased demand for commercial real estate and competition for high-quality assets will cause asset prices to overtake their property values in certain sectors. "The relationship between the value versus price of commercial real estate is precariously balanced," said Ken Riggs, RERC president and CEO in a statement on the report. "Our analysis showed upward pressure on pricing without a corresponding increase in value, and when this happens, investors may be forced to accept lower returns for assets with added risk."  http://www.huffingtonpost.com/mary-ellen-biery/banks-seeing-lower-loss-r_b_5870104.html Shaw Capital Management and Financing provides export trade financing to clients in every major world market and can convert accounts receivable finance transactions in 17 currencies. Avoid scams and other fraudulent transactions. Deal with the best financing companies only. No registration fee needed.

We have no minimum or maximum monthly volume requirements. Other factoring companies require a financial commitment for the amount of freight bills you factor each month. Our highly skilled team provides full administrative support - including credit management, invoicing, collections, account reporting, expense reporting, fuel card management and much more! With Shaw Capital Management and Financing, you get paid in full minus our fee the day we receive your freight bills. Other factoring companies holdback 10 to 15 percent of your money or more for each invoice in a reserve account. That reserve amount is not immediately provided to your company. In the end, you receive part of that percentage back, depending on how long it takes the factoring company to receive payment on the invoice. Shaw Capital Management and Financing factoring process works: 1. Contact us to become Shaw Capital Management and Financing client and be a member, just fillup form available online; 2. You must submit a factoring application for each load you want to factor at least 24 hours before your freight bills arrive in our office. Please request for an Online Application Form If you are on the road without Internet access, a fax version is available upon request; 3. Deliver the shipment, and then send us your freight bills, rate confirmation sheet and all paperwork and; 4. Get paid. We provide same-day-funding when your freight bills arrive. We prepare all invoices on our behalf, submit them and collect payment directly. Avoid scams and other fraudulent transactions. Deal with the best financing companies only. No registration fee needed, secure your money. At Shaw Capital Management - providing a fast, simple and affordable solution to bridge the gap between billing and collections ... Shaw Capital Management and Financing provide same-day-funding. We can help you meet your cashflow needs immediately without entering into a long term factoring relationship. The money you get for the freight bills we purchase is payment in full. Shaw Capital Management and Financing offer a complete line of factoring services, purchase order funding, asset based financing, accounts receivable management, and other related financial services. Shaw Capital Management and Financing offer funding for a wide range of industries and flexible funding requirements that most businesses can easily qualify for. Based in Baltimore, Maryland. Importing into the tri-state area mostly from the far east such as China, Thailand, Taiwan and South Korea. For your convenience, we have associate offices in Shanghai, Hong Kong, Taipei and Seoul in S Korea. At Shaw Capital Management - No financials needed and with Flexible terms. Value of great service... Help grow your business...  Shaw Capital Management and Financing - Whether your item is big, small, fragile, difficult or oversize, no shipping assignment is too big for us. Get in touch with us today for a no obligation quote or estimate, we're here to help. Our estimates include all fees and we take care of everything with a team made up of experienced professionals. No hidden shipping costs. Let us blow away the smoke! Were open, up-front, and we include all costs in our prices. We take care everything. We handle every step of the shipping process. If a problem comes up at any stage, we have the experience to solve it. Were passionate about what we do, and were here to help you in any way we can. http://management.ezinemark.com/shaw-capital-management-and-financing-31ac70cb369.html If you are getting a mortgage, you should settle only for the best deal out there in the market. Find out how you can get a good mortgage deal through this article.

Shopping around for the best home loan rate will help you get the best deal that you want. Remember that a mortgage, whatever form it is, whether it is for a home purchase, home equity or refinancing, is highly negotiable and always changing. It is your task to shop around, compare rates and negotiate to save yourself a few hundreds to even thousands of dollars.  Shop around There are a number of possible lenders waiting to present you their offers - from commercial banks and mortgage companies to thrift institutions and credit unions. These lenders have different rates and offer slightly different kinds of services. The only way to find out what home loan rate each of them has and what type of mortgage they offer is to get in touch with them. Fortunately, you can easily contact them through the Internet. Compare What important information should you get from these lenders? Of course, your foremost consideration will be the home loan rate they can offer you. You can ask whether their rate is adjustable or fixed, and take note how adjustable rates pose a greater amount of risk. Aside from the rate, make sure you also find out the costs involved in the mortgage as well as the monthly amount you need to pay for. When scouting for a good home loan rate and the best deal, you need to ask information on the same loan amount, loan type and term and compare the accordingly. Negotiate Once you have compared various lenders, it is time for you to narrow down your choice into one. Choose your lender based on the information you garnered and contact them for negotiation purposes. Generally, brokers and loan officers are usually allowed some extra compensation when signing in a deal with you. Most of them are fortunately willing to negotiate to give you a much better deal. You can first have your lender write down all the costs that you will need to pay for your loan at the set home loan rate. Based on this list, you can ask your lender to reduce or even waive some of the fees or agree on a lower rate or fewer points. What you want is to get a good deal, so make sure your lender gets away with it by lowering one fee while raising another. Do not be embarrassed to ask your lender to give you better terms than the original ones you were quoted with. You can even cite some offers which you found elsewhere but had to forego when you chose them. Getting the best home loan rate and the best deal when taking on a mortgage is one hard work that you need to exert effort on. You need to spend time and think about how you can come up with better terms. However, each minute you spend is potentially worth it. Who knows, you might just get lucky and save on thousands of dollars through a simple haggling procedure. http://www.articlebiz.com/article/129168-1-tips-in-getting-the-best-home-loan-rate Having a killer business idea is not enough to start a business. 'Finance' is the key factor that is required to start any kind of business - a small business unit or a medium size one. Take time to pen down the various sources/options for financing your venture. This would give you a vague idea regarding whom to approach for a loan. You should also consider how and when you plan to repay the same.

There are certain things that you need to take into consideration, while applying for a business start up loan. First and the foremost thing is to check your credit report. If you have a bad credit history, repair your credit first. A bank or a financial institution will lend you money at a higher rate of interest, if your credit rating is poor. Instead of paying a higher rate of interest, it is wise to improve your credit score, and then approach a financial institution. The Loans You can finance your new business by using some amount of money from your savings. Another source is to borrow from close family and friends. If they have faith in your business plan, they would be ready to finance it. Else, you can apply in any of the traditional financial institutions, for instance a local bank or a Credit Union.  Small Business Administration Small Business Administration or SBA is the single largest organization in the United States to provide assistance to any new venture. SBA assists a new business by granting loan at a reasonable rate of interest. Whatever may be the size of the business, the applicant must contribute at least 10% of the total amount as down payment. The money can be used for various purposes such as to buy machinery, furniture, and could also be used as a working capital. These are long-term programs ranging from 7 to 25 years, and the maximum amount that is lent is around $2 million. Secured Loan You can obtain a loan, if you are ready to provide a collateral. A collateral is an asset such as your car, home, or property, which a borrower pledges with the bank to raise the capital. A secured loan is easy to acquire at a reasonable rate of interest. However, keep in mind that if you default on the monthly payment, the financial institution or the bank has the right to foreclose your property. Bad Credit Business Loan Approaching a bank may not be easy, if you have a blemished credit history. No bank would be willing to give you a loan, if you have a credit score less than 650. A private financial institution usually grants bad credit business loan, but at a higher rate of interest. Before zeroing in on a particular financial institution, check out the online and offline bad credit business loans. This would give you a vague idea regarding the rate of interest offered by various financial institutions. Business Start Up Loans for Women Nowadays, women have become career-oriented. Many of them are interested in starting their own ventures. They can avail business start up loans at a reasonable rate of interest through SBA programs. Most banks and Credit Unions lent money under the SBA program. If a woman is interested in it, she should first approach a nearby bank or the local Credit Union to get more information. Choose the option that is best for you. If you are not sure about how to go about the process of acquiring a loan, do not hesitate to approach a reputed financial adviser. After understanding your business plan, he would be able to guide and also advise you on the type of loan that is best suited for your venture. http://www.buzzle.com/articles/loans-for-starting-up-a-business.html |

RSS Feed

RSS Feed